Somewhere between Amazon letting Chase cardholders knock points off their basket and Walmart's Sparky agent surfacing Walmart+ benefits during AI-assisted checkout, loyalty changed. Redemption stopped being a destination and became a behavior.

That should worry every brand whose loyalty flow still sends customers to a separate rewards page full of thresholds, fine print, and expired motivation. Amazon and Walmart proved something simple: when pay-with-points works well, it doesn’t feel like redemption. It feels like paying a slightly lower price. Once customers experience that, the old earn-and-burn model starts looking exactly like what it is: friction disguised as reward.

Pay with points is a loyalty mechanic that lets customers apply loyalty points directly at checkout, covering part or all of a purchase in real time. Instead of navigating to a rewards catalog, customers see their balance, apply points, and instantly reduce the order total.

Done well, it feels no different than applying a discount code, except the discount is funded by loyalty currency the brand already issued. Done badly, it becomes another loyalty dead-end: minimum thresholds nobody reaches, confusing conversion rates, and redemption rules customers don't understand. The difference between those outcomes is mostly infrastructure.

For years, loyalty programs relied on delayed gratification. Customers earned points first and worried about redemption later. The problem is that “later” often never comes.

A 2025 Euromonitor survey found that 54% of loyalty members redeem rewards at least monthly. Which also means 46% don’t. In many cases, not because they don’t want to, but because redemption still feels like work.

That creates a growing liability for brands. Points sit unused while customers forget they exist, and the brand carries the obligation attached to them long after the original purchase is complete. Customers increasingly expect loyalty value to behave more like wallet credit than collectible tokens, which is why pay-with-points matters. It collapses the distance between earning and using value.

The best implementations also support different customer behaviors at the same time. Some customers want small but frequent discounts, while others prefer saving points for larger rewards later. Most loyalty programs accidentally optimize for only one of those groups.

Amazon's Shop With Points is mechanically simple: connect your Chase, Amex, Citi, or Discover account and apply points at checkout. What matters is the economics underneath.

Chase Ultimate Rewards points redeem at roughly 0.8 cents per point on Amazon, while the same points can often be worth more elsewhere. Amazon trades convenience for conversion efficiency, and millions of customers accept that trade every day without knowing they're making it. That highlights one of the most important design decisions in loyalty: the points-to-cash conversion rate. Most programs still use a single flat rate everywhere, for everyone.

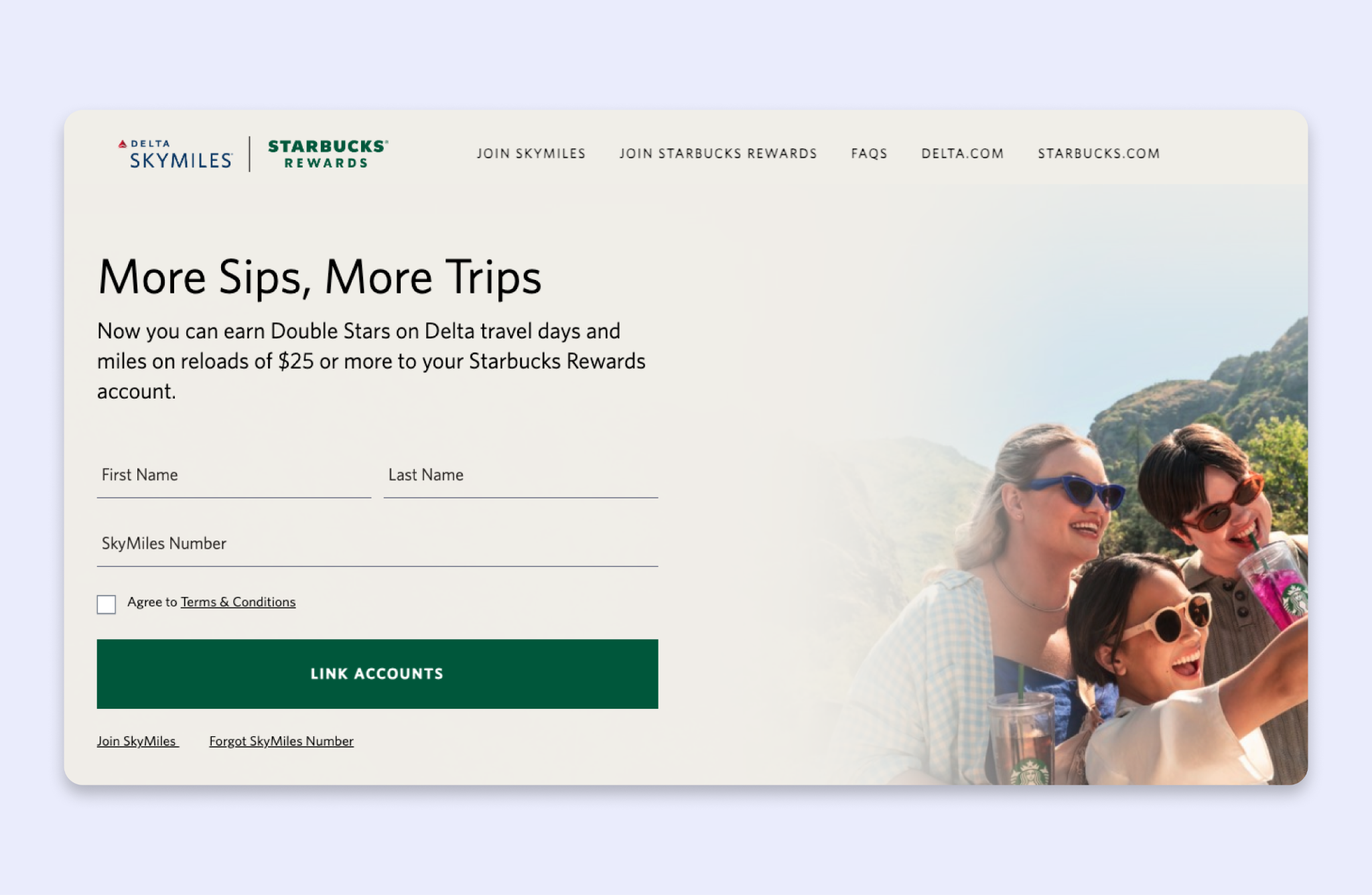

Delta took a different approach. SkyMiles members can convert airline loyalty into Starbucks Stars, creating a cross-brand redemption flow that feels useful in everyday life. Different brands and currencies sit underneath, but to the customer it still feels immediate and simple. That's where multi-currency loyalty starts becoming strategically interesting.

A multi-currency loyalty wallet lets brands manage different point types inside the same loyalty account. A customer might simultaneously hold standard points earned on purchases, promotional bonus points with short expiration windows, and status points that drive tier progression but aren't redeemable.

Rather than one flat balance that earns and burns at a single rate, a multi-wallet setup might look like this:

That changes pay-with-points from a blunt mechanic into a configurable system. Brands can apply different conversion rates per wallet, prioritize which balances get spent first, and offer better redemption rates to VIP tiers without affecting the economics of the entire program.

This is no longer an exotic setup reserved for the biggest loyalty teams. It's the baseline for mature programs that want real control over incentives and customer behavior.

Most pay-with-points discussions focus on UX. The harder problems are operational.

Here's a surprisingly difficult setup for many enterprise loyalty systems: running miles and status points in one program, supporting promotional currencies with separate expiration windows, and applying wallet-specific redemption rates with tier-level overrides.

Most brands end up stitching these capabilities together manually: spreadsheets, custom APIs, parallel programs. The issue usually isn't strategy. It's execution speed. The brands that move fastest tend to win because their infrastructure allows experimentation before competitors even clear internal backlogs.

We rebuilt our loyalty engine from scratch, and pay-with-points is one of the areas where the new architecture makes the biggest difference for teams that have outgrown the old one-rate-fits-all model.

A single loyalty program can hold multiple point wallets, each with its own currency, earning logic, and expiration rules. Miles and status points in one program. Promotional points with 30-day expiry alongside standard annual points. Each wallet operates independently.

Instead of one universal rate, Voucherify supports wallet- and tier-level formulas. Standard members redeem at 100:1, VIPs at 80:1, and promotional bonus points convert differently than standard earned points within the same checkout, same transaction.

Earned points stay locked until conditions like delivery confirmation or return-window expiry are met. Customers see the balance, but can't spend it yet. If the order is returned before activation, the points never become redeemable.

A customer buys three items, earns 300 points, returns one. Voucherify recalculates based on what they kept. No all-or-nothing clawback, no points windfall on returned merchandise. Expiration logic and refund logic work together so partial returns don't create vulnerabilities.

Global limits cap what a member can earn or spend over a period. Transaction limits cap a single interaction. Both run independently across wallets. The double-points-weekend disaster becomes a configuration choice.

Each tier can override conversion rates, reward access, expiration schedules, and spending limits. Platinum members don't just earn faster: their points redeem at better rates and unlock rewards unavailable to lower tiers.

And because the validation layer runs entirely through APIs, the same rules apply whether redemption happens at checkout, in a mobile app, through a third-party integration, or via an AI shopping agent. That consistency is what agent-ready loyalty actually means.

Winning on retention isn't about having the most generous point table. It's about having one that customers can actually use. The programs that get this right aren't doing anything exotic: they've just stopped making redemption feel like a puzzle. No threshold hunting, no conversion rate math, no checkout walls.

A points balance that behaves like cash isn't a nice-to-have. It's the difference between a loyalty liability sitting on your books and a mechanic that brings customers back.