Loyalty used to fit neatly into one balance. Earn points, redeem them, maybe get a birthday gift if the brand was feeling generous. That world is gone.

Today, loyalty programs need to handle points, cashback, store credit, status progression, bonuses, and whatever else the loyalty product owner thought of.

This is why it's the right time to chat about multi-currency loyalty wallets. Because it looks like modern loyalty cannot (or simply won't) run on one balance anymore.

A multi-currency loyalty wallet is a more flexible type of digital loyalty wallet. Instead of one balance, it lets one customer hold different types of loyalty rewards, each with its own rules.

For example, a beauty brand could use stars as spendable points, moons as status credits, and glow points as a seasonal campaign currency. Stars can be redeemed at checkout. Moons move the customer toward the next tier but cannot be spent. Glow points expire at the end of the month. Quite complex, but hopefully you got the gist!

That is the important part: these balances live in one loyalty experience, but they do not behave the same way. The customer sees one loyalty experience. The brand gets separate currencies, separate rules, and cleaner accounting behind the scenes.

Single-balance loyalty wallets look simple until the brand asks for anything remotely realistic.

These are normal loyalty use cases. But on a single-currency wallet, every one of them becomes a costly workaround.

You either create a parallel program, hard-code campaign logic, or send a dev ticket to someone who has better things to do than rebuild the loyalty engine because marketing wants a double-points weekend.

Loyalty point balances are not just an engagement mechanic. In many programs, they represent future value the business may need to honor, i.e. a liability.

If your loyalty wallet treats all points as one undifferentiated balance, you lose control over where that value came from, how long it should live, and what it should be allowed to fund.

Bonus points from a margin-safe campaign sit next to compensation credit issued after a failed delivery. Referral rewards sit next to standard earn points. Seasonal promotional points live forever because the system cannot expire them separately. Then finance asks what the outstanding loyalty liability actually means, and everyone suddenly becomes very interested in spreadsheets.

Multi-currency loyalty wallets make the accounting cleaner because each wallet can carry its own rules. The business can see which balances came from which campaigns, which balances are close to expiration, and which incentives are creating future cost.

Points are not dollars. They live in a different mental account. Customers know, vaguely, that they have some points. But figuring out what those points are worth, where they can be used, whether they expire next month, and whether they meet the redemption threshold is enough friction to make doing nothing feel easier.

The market is moving in the other direction.

Research commissioned by Engage People and conducted by The Wise Marketer among 752 U.S. consumers in August 2025 found that 79% of respondents had used pay with points at checkout. That was nearly double the share reported two years earlier, when 37% had tried it.

Customers are getting used to rewards that behave like spendable value at checkout. Not "go to the rewards page" and "copy this code." Just apply the benefit when the customer is making the decision.

That requires wallet infrastructure that can return a balance in real time, validate eligibility, apply the right currency, and handle partial redemption without slowing down checkout.

Feature checklists are easy to game. These are the capabilities that actually determine whether a loyalty wallet can do what modern programs need.

Most loyalty programs bleed engagement at the same place: the gap between earning a reward and remembering to use it. Auto-redeem eliminates that gap.

Once a customer crosses a defined threshold, the loyalty system issues the reward automatically. The program does the work. Redemption rates go up because the friction point is gone.

On a single-currency wallet, a double-points weekend on top of a seasonal bonus campaign means parallel programs and someone manually cleaning up the mess afterward.

Multi-currency wallets let each currency carry its own earning rules, expiration settings, and spending controls independently. The bonus wallet runs its own logic, while the core program stays untouched.

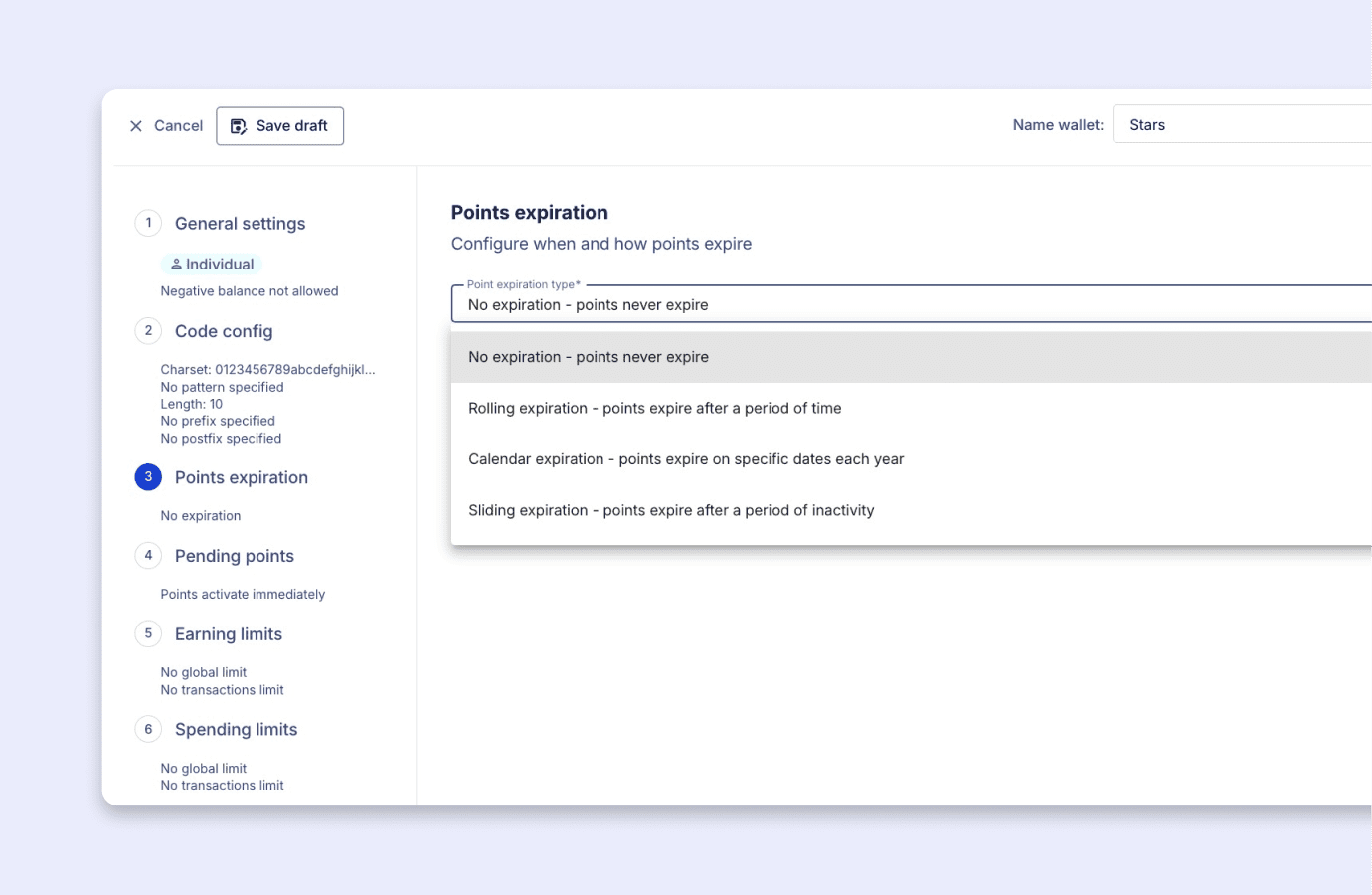

Points that never expire become a liability that never resolves. Points that expire too fast feel punitive and kill program attachment. The three models worth having are rolling (X days from earn date), calendar-based (end of quarter or year), and sliding window (evaluated continuously over a rolling period).

The important thing is configuring them per wallet, not locking one model across the whole program.

Pending loyalty points are earned points that appear in a wallet immediately but cannot be spent until a defined condition is met. Usually that condition is a payment settling, delivery being confirmed, or a return window closing.

A customer buys three items under a free returns policy. Points land in their wallet, visible but not spendable. One item comes back, and the engine recalculates. All three come back, and nothing activates.

A B2B program where employees pool points toward team rewards. A consumer program where a customer gifts their balance to a family member. A multi-brand setup where points earned in one property convert to credit in another. Point transfers make all of this possible without building separate campaigns for each mechanic.

The architecture of a multi-currency loyalty wallet determines everything downstream: what behaviors you can reward, how you handle returns, whether you can run a bonus campaign without wrecking your liability ledger, and whether your loyalty logic is readable by something other than a human.

Most brands treat the wallet as a display layer. The ones pulling ahead treat it as a data structure with business logic attached.

Google's Universal Commerce Protocol (UCP) supports identity linking, which means shoppers can receive loyalty benefits on integrated platforms without leaving them. For loyalty teams, the implication is straightforward: wallet data needs to be available to systems outside the brand's own rewards page.

If your loyalty wallet is a number sitting in a member portal with no API, no real-time validation, and no way to be called by an external system, it won't show up in any of this. For the agentic commerce side, how to optimize incentives and loyalty for AI agents is worth reading alongside this.

Voucherify treats the loyalty wallet as part of the incentive infrastructure, not just a balance display.

That means teams can model multiple currencies, run controlled experiments, and keep the business logic clean as loyalty programs get more complex.

Most loyalty teams are still asking how to make their program more engaging. The better question is whether their wallet can show up where the purchase happens.

Can it return a balance in real time? Validate a redemption outside your own app? Give a shopping agent something useful to work with? If not, engagement strategy is getting ahead of infrastructure.